Global Coffee Trade Flows Analysis: Production and Consumption Patterns Reshaping the Market (2025-2026)

“This report provides an in-depth analysis of the global coffee trade landscape for 2025-2026, highlighting record production driven by Robusta expansion and contrasting trends in Arabica supply. It examines shifting export patterns, evolving consumer preferences, and key market dynamics, offering essential insights for navigating the increasingly complex international coffee market.”

Within the landscape of global agricultural commodities, coffee maintains a uniquely significant position. As the world's most widely traded tropical product, coffee connects the growing belts of the Southern Hemisphere with consumer markets in the Northern Hemisphere, supporting the livelihoods of approximately 25 million farmers worldwide. In 2025, the global coffee trade landscape is undergoing profound transformation: production has reached historic highs, varietal structures continue to diverge, and trade flows are being reshaped by intensifying regional competition and policy adjustments.

I. Global Supply Landscape: Record Production and Varietal Divergence

According to the latest report published by the United States Department of Agriculture (USDA) in December 2025, global coffee production for the 2025/26 crop year is projected to reach a record 178.8 million bags (60kg each), representing a year-on-year increase of approximately 2%. Behind this historic milestone lies a structural shift characterized by robust expansion of Robusta production and concurrent contraction of Arabica output.

Robusta coffee production is estimated to reach 83.3 million bags, a year-on-year increase of 10.9%, primarily driven by capacity expansion in Vietnam, Indonesia, and Ethiopia. In contrast, Arabica coffee production is projected at 95.5 million bags, a year-on-year decline of 4.7%, with major growing regions in Brazil and Colombia affected by adverse weather conditions and cyclical production downturns.

Brazil, the world's largest coffee producer, is forecast to produce 63 million bags in 2025/26, representing a decrease of 2 million bags from the previous year. Within this total, Arabica production is expected to decline by 6 million bags to 38 million bags, as drought and high temperatures significantly impacted flowering and fruit setting in Minas Gerais and São Paulo states. Meanwhile, Robusta production reached a record high of 25 million bags, with abundant rainfall in Espírito Santo and Bahia states supporting fruit development.

Vietnam has consolidated its position as the world's largest Robusta supplier, with 2025/26 production projected to recover to 30.8 million bags—the highest level in four years. Favorable weather conditions and high prices incentivized farmers to increase inputs such as fertilizers, further improving yields. During the first ten months of 2025, Vietnam's coffee exports reached 1.31 million tons valued at $7.42 billion, representing a year-on-year increase of nearly 62%.

Indonesia has emerged as a significant contributor to global supply growth this year, with Robusta production expected to increase by 1.7 million bags to 11 million bags, ranking as the world's third-largest Robusta producer. Sumatra accounts for approximately 75% of Indonesia's coffee production, primarily through smallholder farming, with labor collaboration models ensuring harvest efficiency.

Ethiopia, the birthplace of Arabica, is projected to achieve record production of 11.6 million bags. Over the past three years, more than half of the country's planted area has been replaced with high-yielding coffee varieties, while the promotion of agronomic practices such as post-harvest pruning has contributed to yield improvements. Uganda has also demonstrated remarkable performance, with production estimated at 6.875 million bags, consolidating its position as the world's fourth-largest Robusta producer. Coffee contributes nearly 20% of Uganda's foreign exchange earnings, generating $1.1 billion in 2024.

II. Export Patterns: Regional Shifts and Evolving Competition

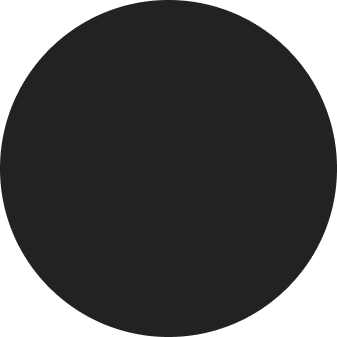

Global coffee exports for 2025/26 are projected to increase to 123.8 million bags, representing an increase of 2.3 million bags from the previous year. Growth is primarily driven by Vietnam, Indonesia, and Honduras, while exports from Brazil and Colombia are expected to decline.

Vietnam's exports are expected to increase by 2.3 million bags to 24.6 million bags, with the European Union serving as its core market. During the first nine months of 2025, Vietnam exported 516,500 tons valued at $2.91 billion to the EU, accounting for 41.5% of its total exports, with Germany, Italy, and Spain as major importers. Tariff advantages under the EU-Vietnam Free Trade Agreement (EVFTA) have further strengthened Vietnam's market competitiveness.

Indonesia's exports are projected to increase by 1.7 million bags to 7.8 million bags, primarily destined for the EU, United States, and Egypt. The EU serves as the primary destination for Indonesian Robusta, while the United States dominates its Arabica imports.

Brazil's exports are expected to decline by 4 million bags to 37 million bags, primarily constrained by low carryover stocks and port congestion. During the first eleven months of 2025, Brazil's coffee exports decreased by 21% year-on-year to 36.9 million bags. However, due to rising prices and an increased share of high-quality coffee, export revenues actually increased significantly. Notably, following the United States' elimination of tariffs on Brazilian coffee, trade flows adjusted: during the August-October period preceding the tariff removal, Brazilian exports to the United States plummeted by 52%, forcing exporters to redirect shipments to Europe and Asia. Germany temporarily surpassed the United States as Brazil's largest coffee buyer.

Colombia's exports are expected to decline by 700,000 bags to 11.5 million bags, primarily destined for the United States and EU markets. Despite a slight decline in production, Colombia maintains its position as the world's leading supplier of washed Arabica, with its quality premium continuing to recover.

African producing regions present divergent performance: Ethiopian exports are projected to increase by 400,000 bags to 7.8 million bags; Uganda and Côte d'Ivoire also recorded growth, while other countries faced challenges. In April 2025, African coffee exports increased by 30.2% year-on-year, marking the 17th consecutive month of growth.

Combined exports from Central America and Mexico are expected to increase by 1 million bags to 14.4 million bags, with Honduras contributing approximately one-third of the region's production.

III. Import Landscape: Western Dominance and Emerging Demand

The global coffee import landscape remains stable, with the European Union and United States continuing as the two core consumer markets.

The European Union, as the world's largest coffee import market, is projected to maintain high import volumes in 2025/26. According to USDA data, EU coffee imports for 2024/25 were revised upward to 46.2 million bags. The EU market is characterized by diverse varietal preferences: Robusta primarily sourced from Vietnam and Indonesia, while Arabica is imported from Brazil and Colombia. In 2025, the EU delayed implementation of the Regulation on Deforestation-free Products (EUDR) until the end of 2026, temporarily alleviating compliance pressure on exporting countries.

The United States, as the world's second-largest coffee importer, is projected to maintain high import volumes in 2025/26. US imports for 2024/25 were revised upward to 23.4 million bags. The US market favors Arabica coffee, primarily supplied by Brazil and Colombia. Adjustments in US tariff policies directly impact trade flows: the elimination of tariffs on Brazilian coffee prompted rapid restructuring of Brazil's export patterns to the United States.

Japan maintains its position as the world's third-largest coffee importer, with annual imports of approximately 372,000 tons. Russia and Switzerland rank fourth and fifth, with imports of 228,000 tons and 210,000 tons respectively. Among emerging markets, China's rapidly growing coffee consumption continues to expand import volumes. Although official data is not reflected in these search results, industry consensus recognizes China as an increasingly important contributor to global coffee trade growth.

IV. Trade Characteristics: Structural Preferences and Price Divergence

Global coffee trade in 2025 exhibits several notable characteristics:

The price spread between Arabica and Robusta continues to widen. In May 2025, the spread between Milds (washed Arabica) and Robusta expanded to 160.09 US cents/lb, a month-on-month increase of 9.3%. This reflects structural market preference for quality-oriented supply. The spread between Colombian Washed Arabica and other Washed Arabicas also expanded from 1.30 US cents/lb to 2.25 US cents/lb, indicating recovery of Colombia's quality premium.

Arabica's share of exports continues to increase. During the 2024/25 coffee year through April 2025, Arabica's share of global exports rose to 63.3%, compared to 59.9% in the same period last year. This structural shift indicates that despite faster Robusta production growth, Arabica maintains a stable position in premium market segments.

Inventory levels continue to decline. Despite record production, global coffee ending stocks are projected to fall to 20.1 million bags, marking the fifth consecutive year of decline. ICE-monitored Arabica certified stocks fell to a 1.75-year low of 398,600 bags, while Robusta certified stocks reached an 11.5-month low. Low inventory levels provide underlying support for prices.

Prices remain at elevated levels. The International Coffee Organization (ICO) monthly composite indicator price has nearly tripled over the past period. In May 2025, the I-CIP averaged 334.41 US cents/lb, representing a decline from earlier highs while remaining at historically elevated levels.

V. Future Outlook: Supply Chain Transformation and Market Restructuring

Looking toward 2026 and beyond, global coffee trade will face multiple variables:

On the supply side, Brazil's 2026/27 production is projected to rebound strongly, with Arabica expected to grow by 29.3% to 47.2 million bags, although Robusta may decline by 8.9% due to weather pressures. Vietnam continues to promote Robusta varietal improvement and irrigation system upgrades, while Indonesia focuses on maintaining stable output. African producing regions' "Coffee Revival Plans" and application of blockchain traceability systems are enhancing their competitiveness in international markets.

On the demand side, global coffee consumption is projected to reach a record 173.9 million bags in 2025/26, representing year-on-year growth of 1.3%. Traditional markets including the EU, United States, and Japan maintain stability, while emerging markets such as China and Southeast Asia present considerable growth potential. Consumer attention to traceability and transparency continues to intensify, driving trade premiums for green and sustainable coffee.

Regarding policy and trade environment, delayed implementation of the EU Deforestation Regulation provides exporting countries with a grace period, although medium-term compliance pressure remains undiminished. Adjustments to US tariff policies may continue to influence regional trade flows. Climate factors remain the greatest source of uncertainty—La Niña conditions may bring drought to Brazil, while typhoons may affect Vietnamese harvests.

From a broader perspective, coffee trade is evolving from the traditional "Southern Hemisphere production, Northern Hemisphere consumption" unidirectional flow toward a more diversified and differentiated pattern. The rise of Robusta is reshaping the varietal supply-demand balance, while technology-enabled solutions and sustainable development are redefining value distribution throughout the supply chain. For international trade practitioners, understanding these structural changes and grasping the shifting dynamics of regional markets will be crucial for maintaining position in an increasingly competitive global coffee trade landscape.