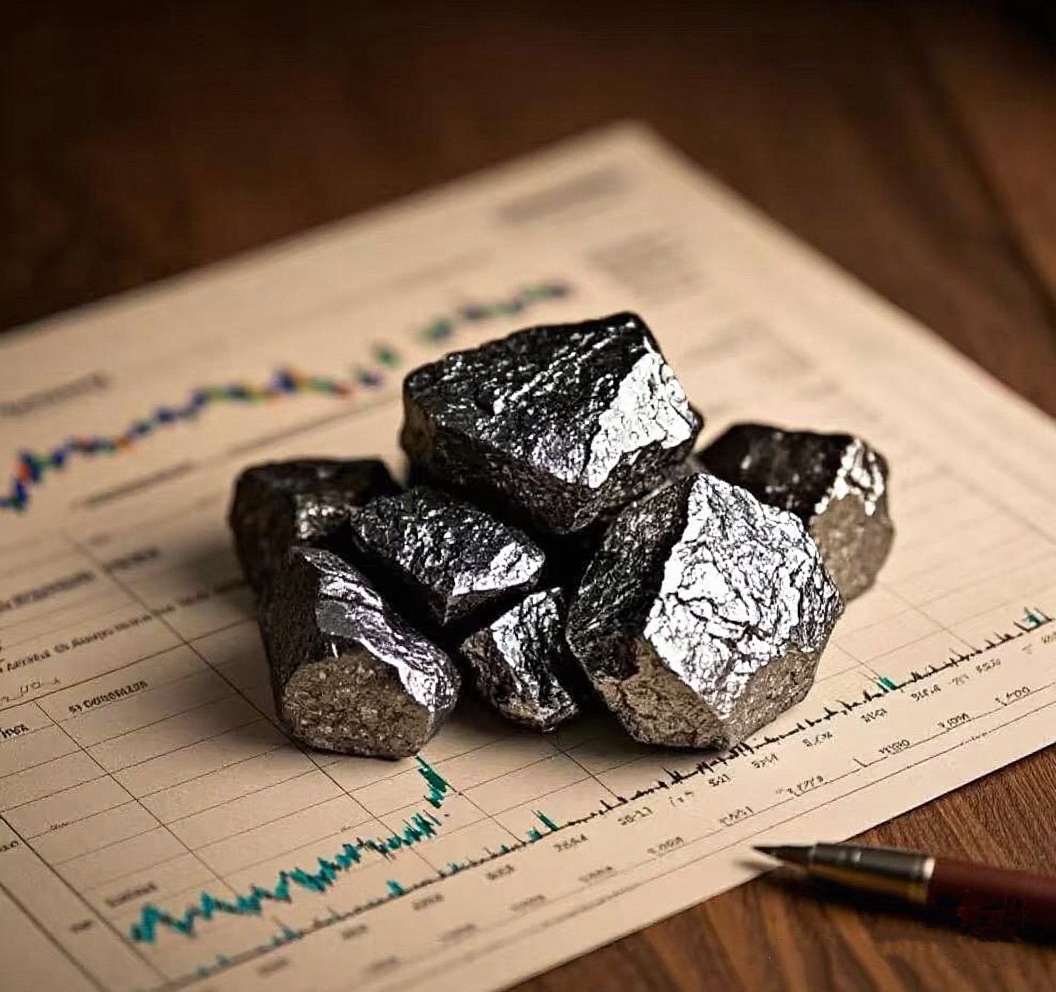

The Great Migration of Global Gold Trade: Why Did 151 Tons of Gold Rush to the U.S.?

“Gold in London vaults is flowing out at an unprecedented rate, while New York on the other side of the globe is becoming the new destination for these precious metal shipments. Behind this silent large-scale migration lies a complex interplay of trade policies, market arbitrage, and the global wave of de-dollarization.”

Gold in London vaults is flowing out at an unprecedented rate, while New York on the other side of the globe is becoming the new destination for these precious metal shipments. Behind this silent large-scale migration lies a complex interplay of trade policies, market arbitrage, and the global wave of de-dollarization.

In early 2025, the international gold market witnessed a remarkable trend: substantial amounts of gold were rapidly moving from vaults in London and Singapore to the United States.

By the end of January 2025, gold holdings in London vaults had decreased by 151 tons (valued at approximately $771.6 billion) compared to the previous month, equivalent to 682,700 gold bars. This shift in trade flows has not only altered the global distribution of gold but also revealed profound changes in the structure of international trade.

01 Three Major Driving Factors: Tariff Threats, Arbitrage Opportunities, and Safe-Haven Demand

This global gold trade movement is primarily driven by three major forces: tariff threats, arbitrage opportunities, and safe-haven demand.

Since the 2024 U.S. election, gold inventories at the COMEX (New York Commodity Exchange) have increased significantly, with nearly 20 million troy ounces of the inflow originating from transfers out of London.

After Trump's return to the White House, uncertainty around his trade policies became the biggest variable for the market. In February 2025, Trump announced plans to impose 25% tariffs on imported goods from countries such as Canada and Mexico, hinting that gold might also be included in the tariff list.

This policy expectation directly triggered a "preemptive stockpiling rush"for gold. To avoid potential future spikes in tariff costs, traders chose to move gold into U.S. warehouses ahead of the policy's implementation.

02 London's Dilemma: Liquidity Crisis and Withdrawal Challenges

The liquidity of London, one of the world's largest gold markets, is being tested. Insufficient liquidity has significantly extended the time required for gold withdrawals, with wait times for withdrawals from the Bank of England's vaults lengthening to 4 to 8 weeks.

This wave of gold migration has substantially reduced liquidity in the London market, making it more difficult to obtain physical gold. At the same time, gold shipments from Singapore to the U.S. also increased notably in January, reaching approximately 11 tons—a record high since March 2022.

03 Arbitrage Mechanism: Widening Spread Between Futures and Spot Prices

The price difference between gold futures on the New York Exchange and the spot market in London once widened to a historic peak of $35 per ounce. This spread stemmed from market panic over potential tariffs and a surge in demand for deliveries on the New York Exchange.

Traders could easily capture arbitrage profits by shipping 400-ounce standard gold bars from London to Switzerland for recasting into 100-ounce bars before shipping them to the U.S. This "cross-market" (cross-market movement) not only accelerated gold flows but also exposed vulnerabilities in the global gold pricing system.

04 The Role of Central Banks: Global Official Institutions' Gold Demand

Central banks worldwide have already joined this "gold rush".According to the World Gold Council, total physical gold demand rose to 4,974 tons in 2024, a record high.

Central banks continued to dominate the gold market, purchasing over 1,000 tons of gold for the third consecutive year in 2024, accounting for approximately 20% of last year's total demand. This trend continued into 2025, with emerging market countries seeking to establish gold-backed trade settlement systems to diminish dollar hegemony.

05 Policy Shift: Tariff Exemptions and New Market Dynamics

It is worth noting that the Trump administration's stance shifted significantly. On August 11, Trump publicly stated that he would "not impose tariffs on imported gold bars."

By September 5, the White House formally issued an executive order exempting key minerals, including gold, from tariffs, effective in the early hours of September 8. This policy change alleviated some market pressure, but the global gold trade landscape had already undergone profound changes.

06 From the Perspective of Trade Professionals: Insights from the Gold Trade Shift

For enterprises and individuals engaged in international trade, the great migration of gold offers important lessons:

★Close attention to policy signals: The Trump administration's repeated adjustments to trade policies indicate that policy uncertainty has become the new normal in global trade.

★Flexible adjustment of logistics strategies: The rapid changes in gold trade flows demonstrate the flexibility of global supply chains.

★Diversified market planning: Changes in gold purchasing behavior by global central banks reflect a trend toward de-dollarization. Businesses involved in foreign trade should consider diversifying currency settlements.

As of June 2025, the U.S. dollar's share of global foreign exchange reserves fell to 58.4%, a 25-year low. The U.S. federal government's debt exceeded $40 trillion, with interest payments accounting for 15% of the fiscal budget.

The direction of gold trade flows is not merely about the movement of the metal itself—it is a barometer of global capital's expectations for the future economy. In the years to come, gold may play a dual role: a safe-haven asset in the short term and a cornerstone of a new monetary order in the long term.