Major Policy Benefit: Cross-Border E-Commerce Export Returns Eligible for "Duty-Free + Refund," New Regulations Explained with Practical Guidelines

“China has introduced a significant new policy for cross-border e-commerce. From 2026-2027, eligible exported goods returned due to overstock or customer returns can be imported back duty-free and with export tariffs refunded, provided they are in their original state. This move aims to reduce business costs and streamline reverse logistics, though strict compliance and documentation are required.”

To stabilize foreign trade development and reduce the burden on enterprises, the Ministry of Finance, the General Administration of Customs, and the State Taxation Administration have recently jointly issued a new tax policy concerning returned goods from cross-border e-commerce exports. The policy clearly stipulates that returned goods meeting specific conditions due to overstock or customer returns, when shipped back into the country, can enjoy exemption from import duties, import-stage value-added tax (VAT), and consumption tax, with a refund of export duties levied at the time of export. This measure aims to address the long-standing pain points of "difficult and costly returns" faced by cross-border e-commerce enterprises, injecting a strong boost for the healthy and sustainable development of the industry.

I. Core Policy Points: Timing, Scope, and Conditions

This policy benefit is not applicable without limits. Enterprises must accurately grasp the following key elements to ensure compliant enjoyment of the preferential treatment:

1.Effective Period: The policy window is from January 1, 2026, to December 31, 2027. Goods that complete the re-import formalities within this period are eligible.

2.Applicable Trade Methods: Only applicable to goods declared for export under Cross-Border E-Commerce Customs Supervision Codes, specifically including:

1210 (Bonded Cross-Border E-Commerce Trade)

9610 (General Cross-Border E-Commerce Trade)

9710 (Cross-Border E-Commerce B2B Direct Export)

9810 (Cross-Border E-Commerce Export via Overseas Warehouses)

3. Return Reason and Time Limit:

Reason: Limited to overstock or customer returns.

Time Limit: Must be returned and enter the country within 6 months from the date of export in their original state. For goods under code 1210, the 6-month period is calculated from the date they left the customs special supervision area or bonded logistics center (Type B).

4.Goods Condition Requirement ("Original State" Definition):

Returned goods must remain substantially consistent with their minimum commodity form at the time of original export.

No addition of accessories, components, or any processing or modification is allowed.

Permitted operations include necessary unpacking, inspection, testing, installation, debugging, etc.

They should in principle not have been used, except for reasonable trial use conducted to verify product quality.

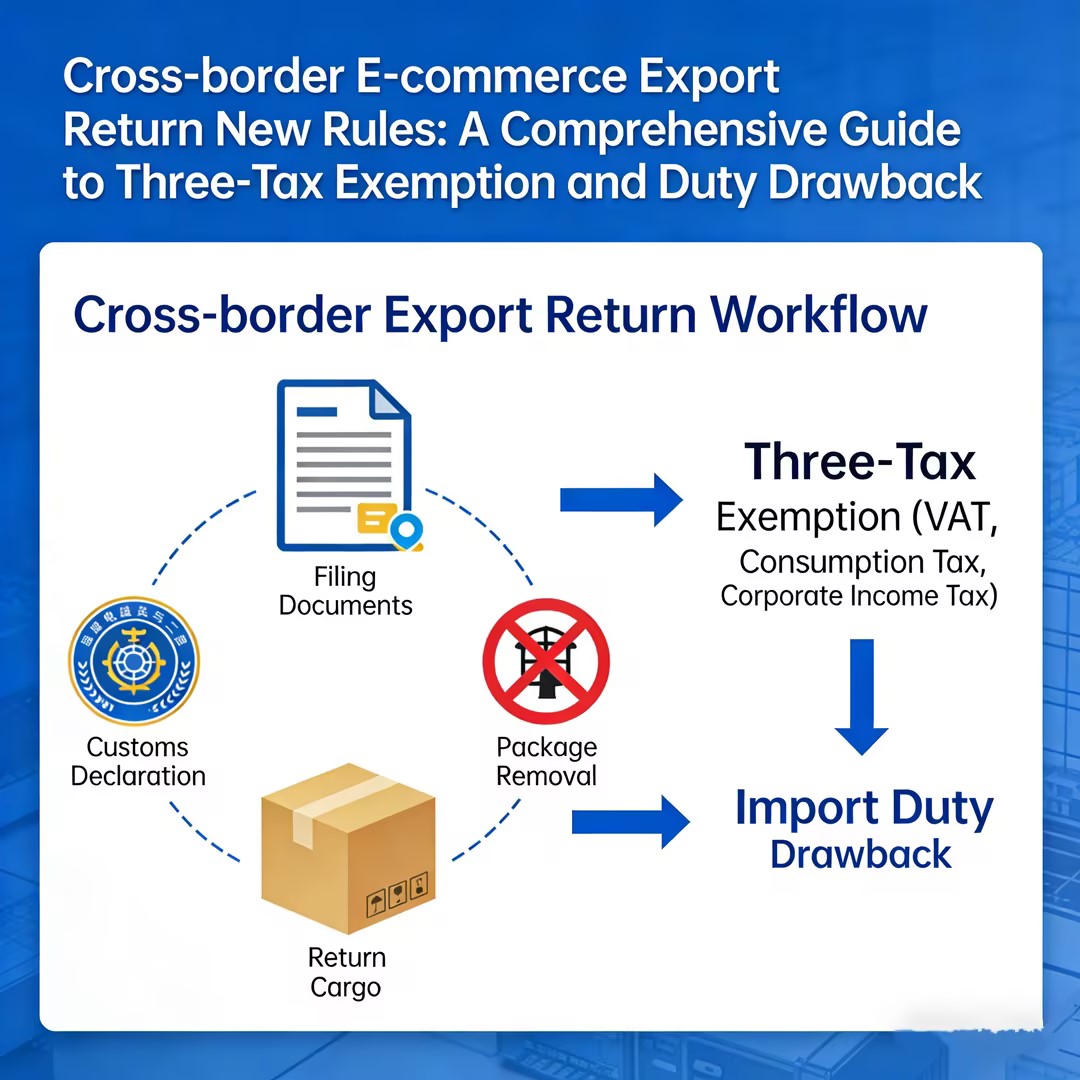

II. Detailed Tax Treatment: "Three-Tax Exemption" and "One-Tax Refund"

The tax benefits of the policy are specifically reflected in two stages: import and export. Enterprises need to handle them separately:

At the import stage, eligible returned goods will enjoy the "three-tax exemption" treatment, namely exemption from import duties, import-stage value-added tax (VAT), and import-stage consumption tax.

The tax treatment at the export stage needs to be distinguished based on specific circumstances:

1.Export Duties: Export duties levied at the time of export will be refunded.

2. VAT and Consumption Tax: Their treatment follows the relevant regulations for returns of domestically sold goods. There is a crucial prerequisite here: if tax rebates were already claimed for these goods upon export, the enterprise must first replenish the rebated taxes according to current regulations. Subsequently, by presenting the "Certificate of Tax Replenishment/Non-Rebate for Exported Goods" issued by the competent tax authority, they can apply for the import-stage duty exemptions and the export duty refund.

III. Enterprise Practical Procedures and Document Preparation

To ensure smooth enjoyment of the policy, enterprises should follow these steps and prepare the required supporting documents:

1.Determine Eligibility: First, confirm whether the returned goods meet the aforementioned requirements regarding time, trade method, reason, and original state.

2.Tax Treatment (Key Preliminary Step):

If tax rebates were processed upon export, the enterprise must first replenish the rebated taxes with the competent tax authority.

Obtain the "Certificate of Tax Replenishment/Non-Rebate for Exported Goods" issued by the tax authority. This document is essential for handling the duty-free and refund procedures.

3.Prepare Return Declaration Documents: When declaring the return to Customs, in addition to routine documents, the following must be submitted:

*Original Export Documentation: Export commodity declaration list or export customs declaration form.

*Proof of Return Reason:

For returns due to overstock: Submit a "Self-Declaration" issued by the enterprise, committing and confirming that the return reason is overstock.

For returns due to customer returns: Submit return records (e.g., screenshots from the e-commerce platform's return backend), customer rejection records, or return agreements, etc.

"Certificate of Tax Replenishment/Non-Rebate for Exported Goods".

4.Customs Declaration and Processing: Use the cross-border e-commerce clearance management system, select the corresponding supervision code for import declaration, submit the complete set of documents, and apply for the duty-free and duty-refund procedures.

IV. Strategic Significance and Risk Control Reminders

The introduction of this policy has profound implications for the industry:

Directly Reduces Enterprise Costs: Significantly reduces the comprehensive tax cost of returned goods, making it financially viable to "return goods," especially beneficial for high-value, high-tax-rate goods.

Improves Capital Turnover Efficiency: Accelerates the return flow and realization speed of inventory, alleviating corporate financial pressure.

Encourages Market Expansion: Reduces trial-and-error costs and risks associated with overseas stockpiling, facilitating more active exploration of new markets and product categories by enterprises.

Optimizes Supply Chain Management: Promotes the integration of forward and reverse logistics, driving the establishment of more refined and flexible global inventory management systems by enterprises.

Important Risk Reminder:

Enterprises bear legal responsibility for the authenticity of their declaration materials and statements. Customs and tax authorities will strengthen supervision over return operations. Acts of tax evasion or fraud through false declaration of reasons or fabrication of returns will be severely punished according to law. It is recommended that enterprises establish sound internal compliance processes, properly archive all transaction, logistics, and return documentation to ensure business traceability and verifiability.

In summary, this policy provides tangible benefits for the cross-border e-commerce industry and represents a significant measure to promote trade facilitation and optimize the business environment. Enterprises should conduct in-depth research, accurately grasp the rules, make full use of the policy window, optimize their operational models, and achieve stable and robust growth.

![[Foreign Trade Updates] Holiday Season Demand Picks Up, Mexico Postpones Tariff Hike, and](/upload/images/2025/11/bbd98c137f34dd0c.jpg)